The federal reserve’s last move in December 2026 nudged the benchmark rate down by a quarter point, sparking speculation across Texas about how soon and how much business loan rates might follow suit. As the economy steadies, lenders are recalibrating their pricing structures while small‑business owners weigh new options from traditional banks to online lenders.

For those navigating this maze, texasloanstoday.com offers a handy comparison tool that highlights current rates and eligibility criteria for Texas‑based borrowers. While the platform itself is a useful starting point, understanding the broader trends behind the numbers can save thousands of dollars over a loan’s life.

The Current Rate Spectrum: Banks vs. Online Lenders

In Q3 2025, the Federal Reserve reported that small‑business bank loans hovered between 6.3% and 11.5% APR. This range reflects the tight credit environment where banks demand solid financials and collateral before extending funds.

- Bank Small‑Business Loans: 6.3%–11.5% APR – source

- SBA‑Backed Loans: Variable: 9.75%–13.25%; Fixed: 11.75%–14.75% APR – source

- Online Term Loans: 14%–99% APR – source

- Merchant Cash Advances: 40%–350% APR – source

The stark contrast illustrates that while banks offer the most favorable rates, they also require a longer underwriting process and often more stringent collateral requirements.

Why Do Rates Span Such a Wide Range?

Several factors converge to create this spread. First, creditworthiness is paramount; businesses with high credit scores and robust cash flows attract lower rates. Second, collateral value can shave 1%–2% off the APR for banks and SBA lenders. Third, market conditions such as inflation expectations influence the prime rate, which directly feeds into loan pricing.

Online lenders, by contrast, operate on higher risk models and compensate with steep fees—sometimes exceeding 99% APR—to cover administrative costs and credit losses. These lenders often serve startups or businesses with less-than-perfect financial histories.

Impact of the Federal Reserve’s December Cut

The Fed’s 0.25% reduction in December 2026 was a modest but meaningful shift for borrowers. Historically, a decrease in the federal funds rate triggers a ripple effect: banks lower their own lending rates to remain competitive, while online lenders adjust their tiered fee structures.

However, the trajectory for 2026 remains uncertain. Recent statements from the Fed’s Board of Governors suggest that future moves will hinge on inflation trends, labor market slack, and global trade dynamics. If inflation cools further, we may see a second cut later in the year; if not, rates could stay flat.

What This Means for Texas Small Businesses

Entrepreneurs looking to refinance or expand should monitor the federal funds rate schedule. A lower base rate can translate into savings of 0.5%–1% on a $100,000 loan—amounting to thousands in annual interest payments.

Moreover, Texas businesses that have built strong relationships with local banks may qualify for specialized SBA programs that offer fixed rates tied to the prime rate, providing predictability in budgeting.

Choosing the Right Loan: Matching Needs to Terms

The type of loan you select should align with your cash flow cycle and growth strategy. Below is a quick reference guide:

| Loan Type | Typical Use | APR Range |

|---|---|---|

| Bank Small‑Business Loan | Capital expenditures, working capital | 6.3%–11.5% |

| SBA Loan | Expansion, equipment purchase | 9.75%–13.25% (variable) |

| Online Term Loan | Quick capital needs, inventory | 14%–99% |

| Merchant Cash Advance | Seasonal sales spikes | 40%–350% |

For example, a boutique retailer in Austin with steady quarterly revenue and solid inventory might lean toward an SBA loan, while a tech startup needing rapid runway could consider an online term loan despite the higher APR.

Fees: The Hidden Cost Layer

Beyond the headline APR, many lenders tack on upfront fees—processing, underwriting, closing costs—that can inflate the Total Cost of Credit (TCC). While banks often keep these fees below 5%, online lenders may charge 10%–20% in upfront charges.

It’s prudent to calculate the Effective Annual Rate (EAR) that incorporates both APR and fees. A simple spreadsheet can reveal whether a seemingly lower APR is actually more expensive once all costs are accounted for.

Collateral: Your Best Ally Against High Rates

Securing a loan with tangible assets—equipment, real estate, or inventory—often unlocks the lowest interest brackets. Lenders view collateral as insurance against default, reducing their risk premium.

- Real Estate: Can secure rates below 6% if the property value exceeds the loan amount by at least 20%

- Equipment Financing: Typically offers 4%–45% APR; the asset itself is the collateral

- Inventory: Commonly used for line‑of‑credit facilities, with rates ranging from 10% to 99%

For Texas businesses, property located in high‑value counties—such as Dallas or Houston—provides stronger leverage. However, the appraisal process can add a few weeks to approval times.

Co‑Signers: A Double‑Edged Sword

Adding a cosigner with strong credit history can reduce rates by 1%–2%, but it also places that individual’s assets at risk if the loan defaults. Many online lenders allow co-signers, but banks typically require them only for borrowers with sub‑prime scores.

Building a Strong Application: The Five Pillars

Lenders sift through applications to assess risk quickly. Strengthening these five areas can shave APR points off the final offer:

- Credit Score: Aim for 720+; check reports for errors and dispute inaccuracies.

- Business Plan: Include market analysis, competitive positioning, and financial projections.

- Revenue History: Demonstrate consistent growth over the past 3–5 years.

- Collateral Documentation: Provide clear titles, appraisals, or inventory lists.

- Personal Guarantees: Offer to personally guarantee the loan if your credit is borderline.

A well‑prepared dossier can cut underwriting time from weeks to days and improve the odds of securing a lower rate.

Leveraging Technology: Loan Comparison Platforms

Platforms like texasloanstoday.com aggregate offers from multiple lenders, allowing you to compare APRs, fees, and repayment terms side‑by‑side. The site also provides educational resources on how collateral affects rates.

While the tool simplifies research, it’s essential to verify each lender’s credentials—look for NMLS registration numbers and read independent reviews before committing.

The Future Outlook: Trends to Watch

As 2026 unfolds, a few macro trends are likely to shape Texas small‑business financing:

- Digital Lending Expansion: AI‑driven underwriting may reduce approval times and broaden eligibility for mid‑size firms.

- Regulatory Shifts: Potential tightening of state-level consumer protection laws could cap maximum APRs for certain online products.

- Economic Recovery Pace: If the U.S. economy rebounds strongly, we may see a gradual decline in the prime rate, nudging overall loan rates downward.

Entrepreneurs who stay informed and proactively manage their credit profiles will be best positioned to capitalize on these shifts.

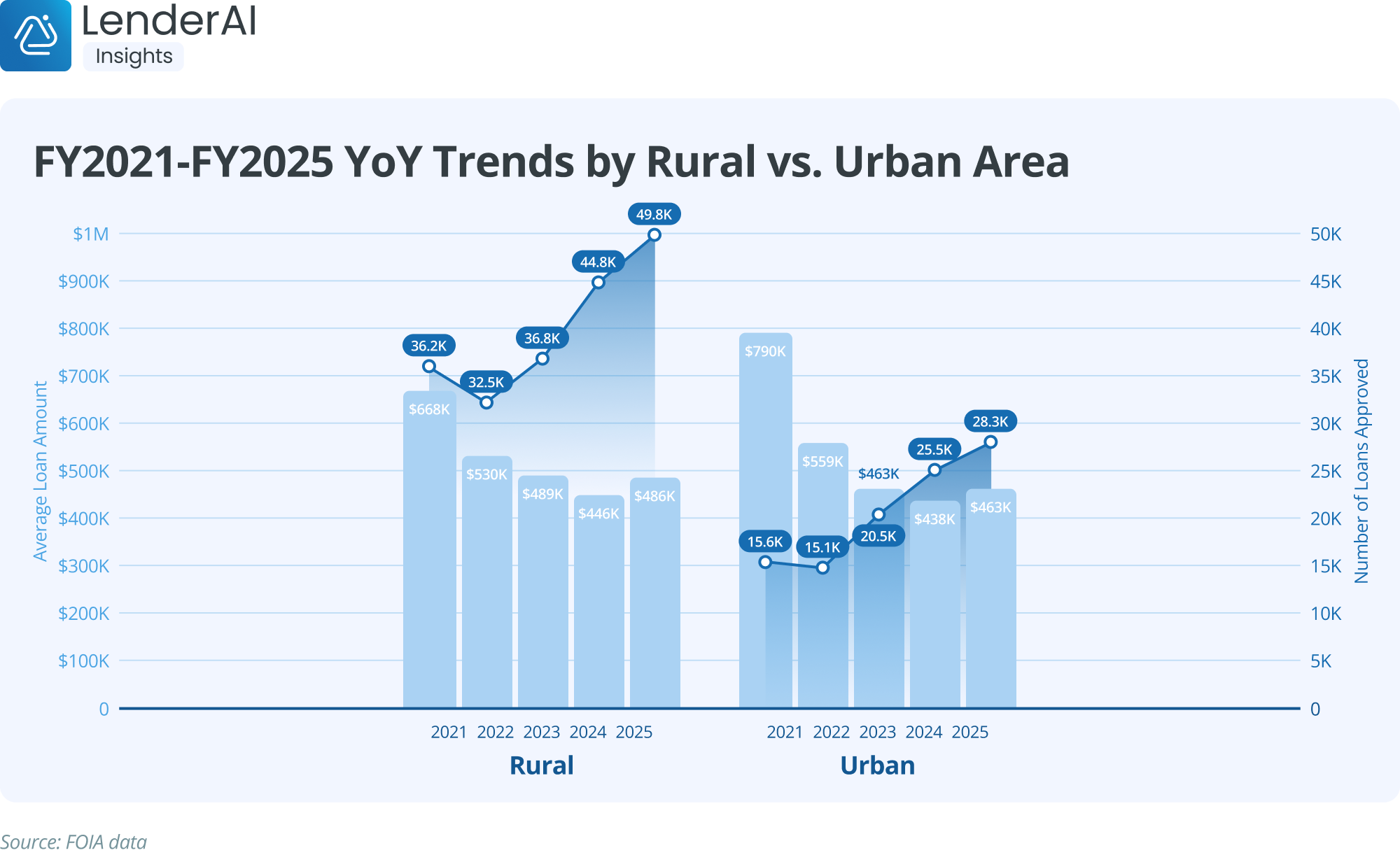

Regional Variations Within Texas

Loan availability and rates can vary significantly between urban centers and rural counties. In metropolitan areas like Houston, Dallas, and Austin, competition among banks leads to tighter rates; meanwhile, smaller towns may rely more heavily on community banks or credit unions with different fee structures.

Local economic development programs sometimes offer subsidized loan options for specific industries—such as renewable energy in the Permian Basin—providing another avenue to secure favorable terms.

Key Takeaways for Texas Business Owners

- Bank and SBA loans generally offer the lowest APRs but require robust financials and collateral.

- Online lenders provide speed and flexibility at the cost of higher rates and fees.

- A 0.25% Fed cut can translate into real savings for borrowers; monitor future Fed actions closely.

- Collateral, a strong credit score, and a polished business plan are your best tools to negotiate lower rates.

- Use comparison platforms like texasloanstoday.com to benchmark offers before applying.

With the right strategy, Texas entrepreneurs can navigate the 2026 financing landscape and secure funding that fuels growth without breaking the bank.